You might have seen the headlines: Google acquires cybersecurity startup Wiz for a staggering $32,000,000,000.

If you're not deep in the trenches of enterprise tech and cybersecurity, your first reaction might be: "Who?" And your second: "Why that much?"

Let's break down the strategic calculus behind this massive deal. It's not just about buying revenue; it's about buying market leadership in a critical battleground, fueled by a unique startup ecosystem, and amplified by venture capital dynamics.

1. The Strategic Imperative: Owning Cloud Security

Think about the major layers of the modern tech stack. Each layer eventually creates hundreds of billions, sometimes trillions, in value, usually dominated by a few key players:

- Networks: Cisco was the historical giant.

- Cloud Infrastructure: AWS, Azure, and Google Cloud Platform (GCP) are the titans.

- Data Infrastructure: Databricks and Snowflake are emerging as leaders.

But here's the key insight: Every infrastructure layer spawns a massive security market. This security layer typically represents about 20% of the value of the infrastructure it protects. Think of it as a necessary "security tax" on building and operating modern technology.

Google Cloud, under Thomas Kurian, understands this intimately. This isn't a new playbook. Kurian previously executed a similar strategy at Oracle, building out a significant database and middleware security business, often through strategic acquisitions of leading startups.

In the cloud infrastructure era, security became paramount. As companies migrated en masse, securing those complex, dynamic cloud environments became a top CISO priority. Several players emerged, but Wiz rapidly established itself as the #1 clear leader in Cloud Native Application Protection Platforms (CNAPP) / Cloud Security Posture Management (CSPM).

Google isn't just buying a company; it's buying the dominant position in securing the cloud – a layer directly adjacent and critical to its core GCP business. Controlling this layer helps protect their existing cloud customers, makes their platform stickier, and gives them a powerful asset to attract new ones wary of complex cloud security challenges. Hence, the $32 Billion price tag for market leadership.

2. The "Unfair Advantage": The Cyberstarts CISO Network

Okay, so Wiz became the leader. But how did they grow so fast, eclipsing competitors and justifying such a valuation in just ~4 years?

Part of the answer lies in a unique early-stage funding mechanism, exemplified by elite Israeli cybersecurity seed investors like Cyberstarts. Their secret weapon? A highly engaged network of Chief Information Security Officers (CISOs).

Here's how the Cyberstarts model reportedly works:

- Talent Pool: It often starts with teams fresh out of elite Israeli military intelligence units (like 8200 or 81).

- Early Validation: The fund connects these nascent teams with CISOs in their network before there's even a product. CISOs share their real-world pain points and unmet needs.

- Incentivized Feedback Loop: CISOs contribute hours for consultation and feedback. In return, they earn points equivalent to carry in the fund (up to ~4% of the GP's carry, according to reports). This aligns incentives – CISOs get potential financial upside for helping shape and adopt relevant solutions.

- Crucial First Sales: This CISO network becomes the source of Wiz's critical first $1M-$10M in ARR. These aren't just any customers; they are influential buyers validating the product. A $100k-$200k deal from a respected CISO can unlock massive valuation jumps.

- Escaping the Grind: As one VC noted, "Until a 'regular' startup company reaches sales of $2–10 million it grinds itself to a pulp, but with this model, this happens in the first year..."

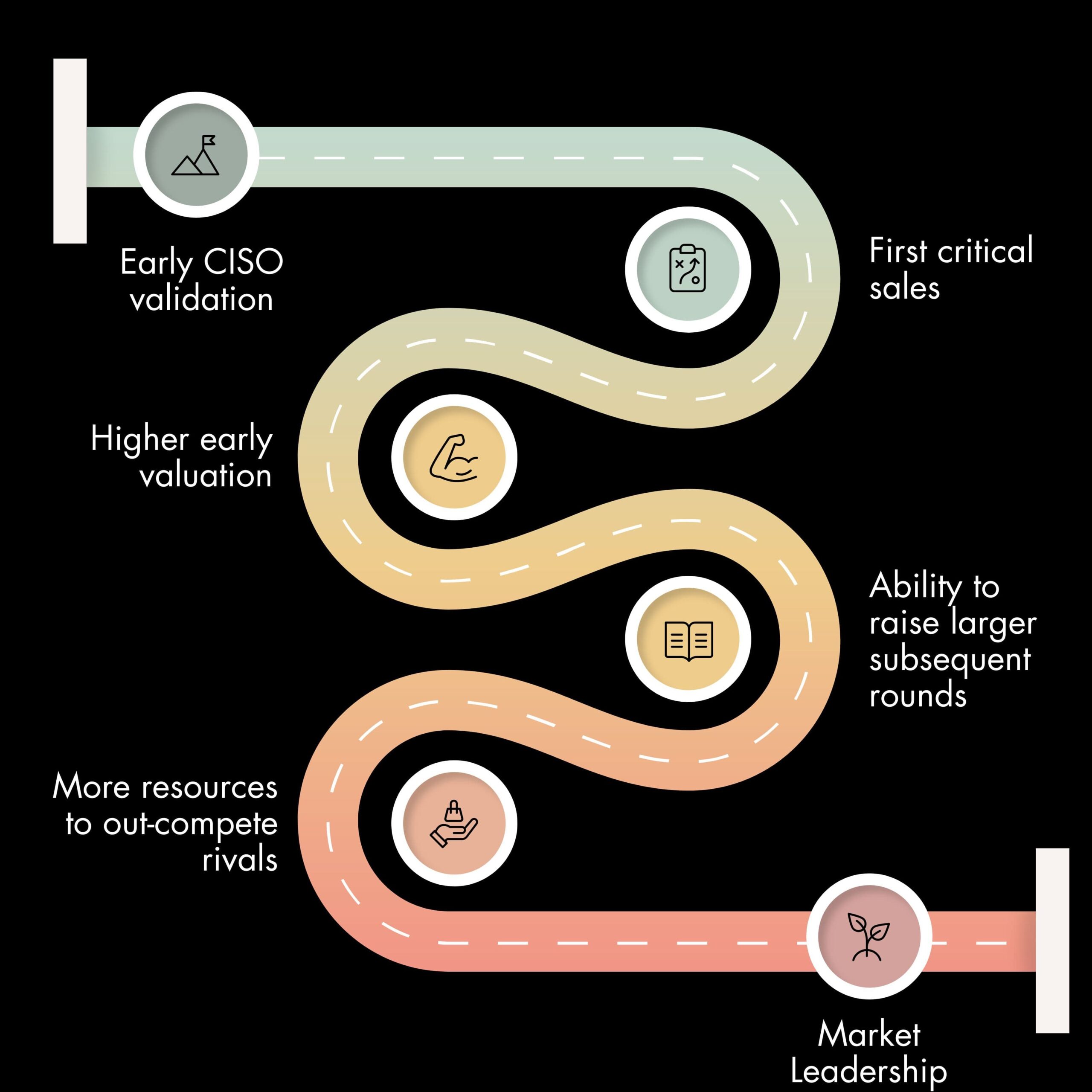

This creates a powerful flywheel:

Early CISO validation -> First critical sales -> Higher early valuation ($100M-$200M+) -> Ability to raise larger subsequent rounds -> More resources to out-compete rivals.

Cyberstarts reportedly owned ~4% at exit, translating their seed investment into ~$1.3 Billion – a >320x return. That's the power of combining elite talent with a built-in market validation and customer acquisition engine.

3. VC Math: Understanding the $32 Billion

Does the $32B price only reflect Wiz's current revenue multiples or strategic value? Venture capital dynamics played a role too. Consider this simplified VC valuation example:

- Round A: An investor puts $80M into Company X at an $800M valuation.

- Round B (a year later): The same investor might participate or lead, putting in another $300M at a $3 Billion valuation.

- On Paper: The investor has now put in $380M total ($80M + $300M). Their initial $80M stake is now marked based on the new $3B valuation. If that stake represented 10%, it's now marked at $300M. Add the new $300M investment (marked at cost), and the total paper value suddenly becomes ~$600M. The valuation escalated rapidly on paper, driven by subsequent rounds.

- The Exit: When the acquisition happened at $6.5 Billion (more than double the last round's valuation in this example), that $380M total investment turned into a significant return (perhaps ~$1.2 Billion, depending on the exact ownership percentage accrued across rounds).

While not a "pyramid scheme" in the illicit sense, later rounds at higher valuations demonstrably inflate the paper value of earlier investments. The $32 Billion acquisition price for Wiz serves as the final validation point for all previous rounds, locking in returns for investors like Cyberstarts (massive multiples) and later-stage funds (still very strong returns). Google is paying a price influenced not just by Wiz's standalone metrics but also by the capital structure and valuation expectations set by the venture funding process.

What's Next? Follow the Infrastructure.

The playbook repeats. If cloud infrastructure created the need for Wiz, what's the next major layer demanding its own security paradigm?

All signs point to data security for the modern AI data stack. As companies build massive data lakes, warehouses, and vector databases to power AI/ML models, securing the sensitive data within becomes the next frontier. We're already seeing startups emerge here, focusing on discovering/monitoring sensitive data or, like our portfolio company Skyflow, fundamentally securing the data itself via techniques like data privacy vaults.

The Wiz acquisition is a landmark deal, highlighting the immense value of category leadership in security. It underscores the power of strategic M&A in the cloud wars, showcases unique ecosystem advantages like Israel's cybersecurity startup engine, and reflects the potent dynamics of venture capital scaling. Keep an eye on that "20% security tax" – wherever infrastructure value congregates, a multi-billion dollar security opportunity is sure to follow.